.jpg)

Are Rental Properties still a Good Investment with Higher Interest Rates?

There are a lot of theories and processes out there available to teach the new Real Estate Investor the tricks of the trade or the seasoned investor some newer ideas that have shown to be successful. When investment property mortgage rates can range from 50 to 87.5 basis points higher than a primary home, according to lendingtree.com, is investment property still a good investment?

According to an article published by bigger pockets, it states that one of the most valuable tools rental property investors in the U.S. is a 30-year-fixed rate mortgage. We all know that this fixed rate is great for allowing investors alike to avoid those unexpected rate hikes down the road but there is another benefit most don't realize is that there are notable periods where these fixed rates are incredibly low making the cost of borrowing money almost trivial.

So, the big question is what happens when those interest rates increase, potentially to levels we aren't used to seeing? Abruptly monthly mortgage payments are distinctly higher, which has a negative impact on your cash flow and returns. Should we slow down on investing in rental properties? How can you counter higher interest rates to stay profitable with your rental properties?

The best way to determine this is by understanding how rental properties make money, the factors you can control in your investments and its profits. Additionally, knowing what to look for in a prospective rental property to help set you up for the greatest chance of successful returns despite the higher mortgage payments.

_1.jpg)

Rental Properties are Long-Term Investments

The number one thing to remember as an investor is that Investment Properties (Rental Homes) are long-term investments. This is not a get rich overnight scheme. Yes, some investors may see a quick equity profit through improvements or value add-ons, and some may land what we are now calling "unicorns" with significant cash flow from the start. Please keep in mind as a general rule of thumb, rental investments see the most profit over the long haul.

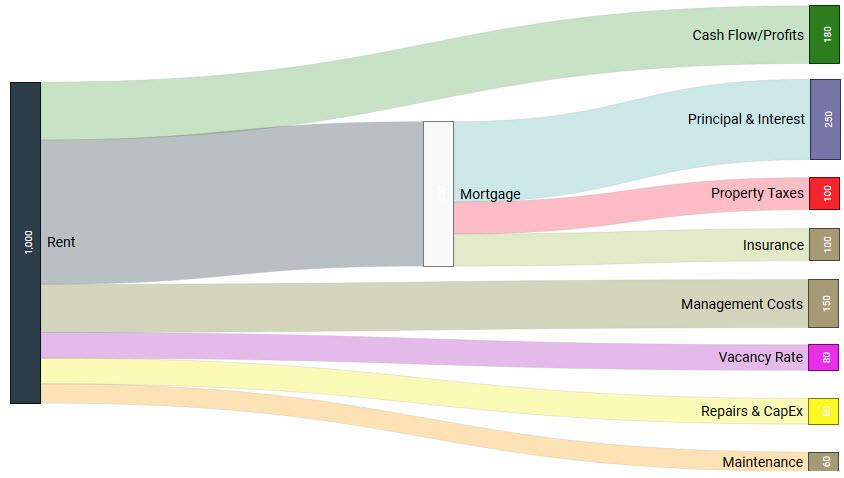

As investors, when we analyze a property's finances to see if it is that great deal we are seeking, often we only see the cash flow numbers that are right in front of us, we don't look or consider the projected cash flow. The immediate number doesn't account for rental increases over time (hopefully while maintaining a fixed mortgage payment), appreciation, demand and inflation. All of those factors continuously change, hopefully for our benefit.

How will your Rental Investment Make Money?

Even before you were an expert in Real Estate Investing, you knew that Rental Property can be very profitable but maybe you didn't quite understand how they can be so profitable.

The five (5) ways that your rental property can make money are:

(1). Cash Flow

(2). Appreciation

(3). Tax Benefits

(4). Equity Built vs. Mortgage Paydown

(5). Hedging Against Inflation

When you truly understand the importance and details of each one of these profit centers, you not only become wiser about the power of holding a rental property for the long-term instead of the short-term, but you also begin to realize that the expense of an interest rate that's a couple of points higher than what your used to likely doesn't hold a candle to the profit potential over the lifetime of the rental property.

You may be thinking "But those other profit centers are speculative and cash flow is still very important and the higher the mortgage expense increases my risks by lowering my cash flow." Yes, and that can be very well true, but what you want to do in this situation to still be successful are two things:

1. Learn to balance the profit centers.

1. Learn to balance the profit centers.

If your cash flow is down due to interest rates, look for another profit center with potential. Examples: maybe you buy in a gentrifying high demand-area, so you can assume that appreciation potential is very high. Or perchance you're investing during a time of extremely high inflation. What could you do in that situation? It is easy to visualize a bar graph with a bar for each of the main profit centers. If one is down, are any of the others up? If they're all down, that's a problem. If some are higher than usual, do those balance them? All of it depends on your unique situation.

2. Put Your Main Concentration on Demand and Location.

One of the keys to investing is investing in properties that will lend their hand to the appreciation bar, as well as inflation and rent demand. As long as people desire the property they own, the greater the profit potential from the profit centers will be and more likely to increase over time. Meaning no matter what area or grade your investment falls under if you maintain the maintenance and overall appearance as if you were going to be occupying the home, then the demand for the home increases.

As an investor, when you truly understand how rental properties make money, it is then when you can genuinely wear the investor hat rather than the consumer hat. It is the consumer's hat that causes people to think that increased interest rates are deal-breakers, whereas individuals who honestly understand how rental properties profit will not only learn how to see how to look past the interest rates but also provide perspective on how to compensate for it.

Lease Escalation

Lease escalations also known as rental increases, are conducted for two reasons: appreciation and inflation. Do you know what doesn't increase over time and is not negatively impacted by appreciation or inflation? Your mortgage payment when you have a fixed-rate mortgage.

This means that your cash flow will continue to grow over the life of your rental home as you continue to increase rents. Increasing rents doesn't have to cause a vacancy if done correctly. Residents are only guaranteed the current rate for the term of the lease, when it is time for renewal increasing the rents at a modest rate of 3-5% often times will not create a vacancy and if it does, the Resident was probably already looking to move anyways. Some areas you will see a 10% annual increase, however you will need to check with your state and local laws as some areas have a cap on how much you can increase and how often or hire a Professional, we are trained to know that and keep up on the regular changes to those statues.

Your expenses, such as property tax and insurance, may increase over time, but they're unlikely to increase at a rate anywhere near what your rents will increase. Overall, you'll see that rents will continue to pull farther and farther away from your fixed-rate mortgage expense and your profits should continue to grow exponentially. When you are looking for a new investment property consider future rents as part of your plan and cash flow to really see the value.

_4.jpg) Profit Increases and Lowering Expenses

Profit Increases and Lowering Expenses

While the emphasis has been on the long-term investment, there are proactive things as an owner/investor that you can do to create more equity faster.

- Improving Your Investment Property: The more desirable your property, the more value it will generate and the more demand it will drive. While most profit centers kick in on their own over time and increase the property's value and rents, you can also make improvements to your investment that will increase desirability and force those profits more rapidly.

- The most basic way of improving your investment is by rehabbing it. When you upgrade your property making it nicer and more attractive, you not only increase value of that property, but the rents and demand increases as well. You are merely speeding along those profits past what a higher interest rate would cost.

- Refinance your mortgage: Keep in mind that the higher interest rate doesn't have to be forever. Mortgage interest rates fluctuate, just as property value and rents do. If interest rates drop lower than your current rate, you can refinance the loan at that lower rate. Obviously, there is no guarantee that interest rates will drop lower than your current fixed rate, but if they do, you can make that move and increase your overall cash flow.

- Location, Location, Location: We have said many times already that location matter and it does! Buying in a path of demand to ensure appreciation potential is key. You can make strategic moves when you learn how to analyze neighborhoods and identify areas with an extremely high chance of appreciation. Forces like gentrification, population growth and job growth are all determining factors that can predict value increases.

- Banking specifically on gentrification, as with any type of appreciation, is speculation at best. You want to educate yourself on how to identify areas that may experience a gentrification impact, but always have a back-up plan in case gentrification doesn't occur. You never want to have all of your eggs in one profit center basket, there is no room for error and that basket may tip. However, if you buy at the right time (meaning you move quickly, you cannot hesitate otherwise you the deal will disappear), gentrification can force an increase in profits.

Going Up Against Inflation

While inflation impacts most areas of our lives negatively, the one place that it helps is with investing in rental properties. Your fixed-rate mortgage expense stays the same for the loan term despite what happens to the value of the dollar. You pay back a loan with yesterday's dollar not tomorrows.

When inflation is compared to the interest rate of the mortgage, many experts argue that the mortgage interest that is paid over a 30-year fixed term is less expensive than paying for the same property in cash with today's dollar due to inflation.

When inflation rate is higher than the interest rate on your mortgage, your profits will continue to outrun the expenses on your mortgage.

.jpg)

Key Points to Remember

It is easy to read this blog and its tips in it and think if you buy and hold a rental investment for a long period of time, it will be profitable because no matter what your expenses may be today, everything will catch up and shift into a profit eventually.

As great as that sounds, it will not be true for every investment. Not all investment properties are profitable and there are many factors that can challenge the various profit centers. It is very important to remember that speculation doesn't always pan out, and you should avoid speculation more often than not.

The idea for this blog isn't to mislead you or misinform but to provide the reader another way to analyze potential investment properties with the understanding that higher interest rates doesn't eat as much of your income as one typically believes.

It's also important to remain educated. Thus, what you believe is a high-interest rate may be "normal." We as a nation have become so used to seeing the historically low-interest rates. We've been spoiled and it misleads us to believe that we can only be profitable if we have crazy low interest rates on our mortgages. We forget when there was a time not too long ago where mortgage rates were all over 10%.

Another way to decrease your payment and possibly that stressful interest rate is to consider putting down a larger down payment.